London St. Pancras Highspeed’s route operations and maintenance (O&M) income and expenditure for the year is summarised in Table 4.1. Please note that some figures in this chapter may not sum due to rounding.

Table 4.1 Summary of London St. Pancras Highspeed’s route operations and maintenance income and expenditure 1 April 2024 to 31 March 2025, compared to PR19 forecast and previous reporting year

| £million, 2024-25 prices | Actual | PR19 forecast | Difference better / (worse) | 2023-24 |

|---|---|---|---|---|

| Income | ||||

| O&M | 86.5 | 73.6 | 13.0 | 81.5 |

| Pass-through income | 25.0 | 25.8 | (0.9) | 26.5 |

| Total income | 111.5 | 99.4 | 12.1 | 108.0 |

| Controlled track costs | ||||

| Network Rail (High Speed) | 54.3 | 54.9 | 0.6 | 54.5 |

| London St. Pancras Highspeed | 12.8 | 11.5 | (1.3) | 12.9 |

| Network Rail Infrastructure Ltd | 2.1 | 2.1 | 0.0 | 1.8 |

| Other | 2.5 | 2.9 | 0.5 | 2.0 |

| Total controlled track costs | 71.8 | 71.5 | (0.2) | 71.3 |

| Pass through costs | ||||

| Rates | 11.2 | 11.6 | 0.4 | 11.1 |

| UK Power Network fees and renewals | 7.7 | 7.7 | 0.1 | 7.3 |

| Insurance | 4.0 | 4.1 | 0.1 | 3.8 |

| Power-non traction | 3.6 | 2.4 | (1.2) | 4.5 |

| Total pass-through costs | 26.5 | 25.8 | (0.7) | 26.5 |

| Freight costs | ||||

| Network Rail (High Speed) | 0.1 | 0.1 | 0.0 | 0.1 |

| Network Rail Infrastructure Ltd | 0.2 | 0.2 | 0.0 | 0.2 |

| London St. Pancras Highspeed | 0.1 | 0.1 | 0.0 | 0.1 |

| Total freight costs | 0.4 | 0.4 | 0.0 | 0.4 |

| Upgrades (cost of ERTMS early works specified upgrade) | 0.4 | 0.0 | (0.4) | - |

| Total O&M costs | 99.2 | 97.8 | (1.4) | 98.2 |

| Performance related payments | 0.0 | 0.0 | 0.0 | |

| Total costs | 99.2 | 97.8 | (1.4) | 98.2 |

| Net income / (expenditure) | 12.4 | 1.6 | 10.8 | 9.8 |

Source: London St. Pancras Highspeed AMAS, 1 April 2024 to 31 March 2025 and 1 April 2023 to 31 March 2024

Income

London St. Pancras Highspeed received £111.5m of route O&M and pass-through (that is, to recover certain costs such as for the use of traction electricity) income this reporting year, £12.1m higher than assumed in its PR19 forecast.

Table 4.2 Summary of London St. Pancras Highspeed’s route income 1 April 2024 to 31 March 2025

| £million, 2024-25 prices | Actual | PR19 | Difference better / (worse) | |

|---|---|---|---|---|

| International | O&M | 33.9 | 25.9 | 8.0 |

| International | Pass-through charges | 6.9 | 7.5 | -0.6 |

| International | Total | 40.8 | 33.5 | 7.4 |

| Domestic | O&M | 52.3 | 47.4 | 4.9 |

| Domestic | Pass-through charges | 18.0 | 18.3 | -0.2 |

| Domestic | Total | 70.3 | 65.7 | 4.6 |

| Freight | O&M | 0.3 | 0.2 | 0.1 |

| Freight | Pass-through charges | 0.0 | 0.0 | 0.0 |

| Freight | Total | 0.3 | 0.2 | 0.1 |

| Total income | 111.5 | 99.4 | 12.1 |

Source: London St. Pancras Highspeed AMAS, 1 April 2024 to 31 March 2025

Income from route O&M charges

£86.5m of London St. Pancras Highspeed’s income was from charges to train operators for operating and maintaining its network. There are agreed chargeable journey times for each service group at a rate per minute or per km per train. These charges, together with train numbers, drive the revenue. Overall, income from O&M charges excluding pass through income was £13m above the CP3 forecast due to £8m higher recovery on Eurostar train service paths and £4.9m higher recovery on Southeastern’s train services following charging reopeners to reflect actual train volumes, plus £0.1m higher recovery costs for freight. There was £0.9m less from pass through income.

An element of route OMR charges is designed to build up a fund to pay for future renewals resulting from today’s wear and tear of the network. This is deposited in an escrow account which is then permitted to be invested, within parameters set out in the Concession Agreement. Both passenger train operators on the network were offered a temporary route escrow payment holiday from Period 1 of 2020/21 to Period 3 of 2021/22. This offer was accepted by Eurostar who deferred around £15.7m of payments into the escrow account which has been repaid with interest in CP3.

Expenditure

Controlled track costs

The majority of London St. Pancras Highspeed’s route costs (£54.3m of a total of £99.2m) were incurred in operating and maintaining its network through a long-term, fixed price contract with NR(HS).

Table 4.3 provides a breakdown of NR(HS)’s costs.

The Operator Agreement between London St. Pancras Highspeed and NR(HS) requires the former to pay train operators if NR(HS) outperforms our PR19 financial assumptions in years 3, 4 and 5 of a control period. The formula requires NR(HS) to make significant savings before having to share the outperformance, so a material outperformance share with train operators requires substantial savings. In this reporting year NR(HS) underperformed by £1.2m and therefore no payments are required to be shared with train operators.

Table 4.3 Network Rail (High Speed) costs 1 April 2024 to 31 March 2025, compared to PR19 forecast and previous reporting year

| £million, Feb 2024 prices | Actual | PR19 | Difference better / (worse) | 2023-24 |

|---|---|---|---|---|

| Staff costs | 27.1 | 25.1 | (1.9) | 24.7 |

| Plant & materials | 7.1 | 7.2 | 0.1 | 6.2 |

| Overheads | 5.6 | 4.4 | (1.1) | 6.1 |

| Corporate functions & Network Rail Infrastructure Ltd | 3.8 | 4.9 | 1.1 | 3.9 |

| Sub-contractors | 3.7 | 3.1 | (0.6) | 3.4 |

| Consultancy costs | 1.8 | 0.6 | (1.2) | 1.5 |

| Security of infrastructure | 1.9 | 2.5 | 0.6 | 1.8 |

| Insurance | 0.8 | 0.9 | 0.1 | 0.6 |

| Operating costs | 51.8 | 48.8 | (2.9) | 48.2 |

| Management fee | 3.9 | 3.9 | 0.0 | 3.9 |

| Risk premium | 0.4 | 2.1 | 1.7 | 5.0 |

| Over/under performance | (1.2) | 0.0 | (1.2) | (2.6) |

| Total NR(HS) costs | 54.9 | 54.9 | 0 | 54.7 |

Source: NR(HS) Outturn statements, 1 April 2024 to 31 March 2025 and 1 April 2023 to 31 March 2024

London St. Pancras Highspeed’s internal costs are shown in Table 4.4. This was £12.8m for the year, £1.3m higher than forecast at PR19. Whilst staff costs have been reduced from last year and are aligned with the CP3 forecast there was an overspend on technical consultant costs due to the additional legal costs arising from PR24 process and proposed PAT changes and overspend on R&D due to catch up of underspends in earlier years of CP3.

Table 4.4 London St. Pancars Highspeed’s internal costs 1 April 2024 to 31 March 2025, compared to PR19 forecast and previous year

| £million, 2024-25 prices | Actual | PR19 forecast | Difference better / (worse) | 2023-24 |

|---|---|---|---|---|

| Staff costs | 6.2 | 6.2 | 0.1 | 6.8 |

| Technical support / consultants | 1.8 | 1.0 | (0.8) | 2.2 |

| Office running costs | 1.6 | 1.7 | 0.1 | 1.6 |

| R&D | 1.4 | 0.5 | (0.8) | 0.3 |

| Other costs | 1.8 | 2.0 | 0.2 | 1.9 |

| Total London St. Pancras Highspeed costs | 12.8 | 11.5 | (1.3) | 12.9 |

Source: London St. Pancras Highspeed AMAS, 1 April 2024 to 31 March 2025 and 1 April 2023 to 31 March 2024

Pass-through costs

Some of London St. Pancras Highspeed’s costs are passed straight through to train operators by offsetting pass-through income. This year the OMRC income includes an adjustment for prior years, correcting past overstatements. As a result, pass through income and cost figures no longer match. The cost line best reflects actual OMRCC costs and income recovered in the year. These costs are largely uncontrollable by London St. Pancras Highspeed and include non-traction electricity costs, business rates and insurance. Pass-through costs were £26.5m this year, which represented underperformance of £0.7m against PR19 assumptions. This underperformance was mainly driven by a £1.2m overspend on non-traction power due to increased electricity costs.

Freight costs

London St. Pancras Highspeed incurs costs relating to freight traffic, including maintaining freight-specific infrastructure, which it passes through to operators through OMR charges. Freight costs were £0.4m, which was in line with the PR19 forecast.

Upgrades

The European Rail Traffic Management System (ERTMS) is a large signalling project that London St. Pancras Highspeed anticipates implementing in CP5 (the five-year control period which starts on 1 April 2030), as a ‘Specified Upgrade’ The Concession Agreement defines certain expenditure as Specified Upgrades or upgrades to the route infrastructure. Specified Upgrades and upgrades may be financed either through a grant from the Government, an increase in the Investment Recovery Charge known as an Additional Investment Recovery Charge (AIRC) or a combination. In the year £0.4m was spent on upgrades and was recovered via additional IRC.

Income and expenditure in CP3 compared to PR19

This report covers the last year of CP3. The following sections summarise the overall financial performance for the whole, five-year, control period. Further details and narrative on what happened during each year can be found in our previous annual reports.

Over the control period, London St. Pancras Highspeed received £470.7m of route O&M income, £2.3m lower than assumed in PR19. It spent £475.7m operating and maintaining its route infrastructure, £1m higher than target.

Table 4.5 Summary of London St. Pancras Highspeed’s route income and expenditure in CP3, compared to PR19 forecast

| £m, 2024-25 prices | Total CP3 | PR19 | Difference better/(worse) |

|---|---|---|---|

| O&M income | 349.2 | 350.4 | (1.3) |

| Pass-through income | 121.6 | 122.6 | (1.1) |

| Total income | 470.7 | 473.1 | (2.3) |

| Total controlled track costs | 350.2 | 349.6 | (0.6) |

| Total pass-through costs | 123.2 | 123.0 | (0.2) |

| Total freight costs | 2.0 | 2.0 | 0.0 |

| Upgrades (cost of ERTMS early works specified upgrade) | 0.4 | 0 | (0.4) |

| Total O&M costs | 475.7 | 474.7 | (1.0) |

| Performance related payments | 0.1 | 0.0 | (0.1) |

| Total costs | 475.7 | 474.7 | (1.0) |

Source: Analysis of London St. Pancras Highspeed AMAS data 2020-2025

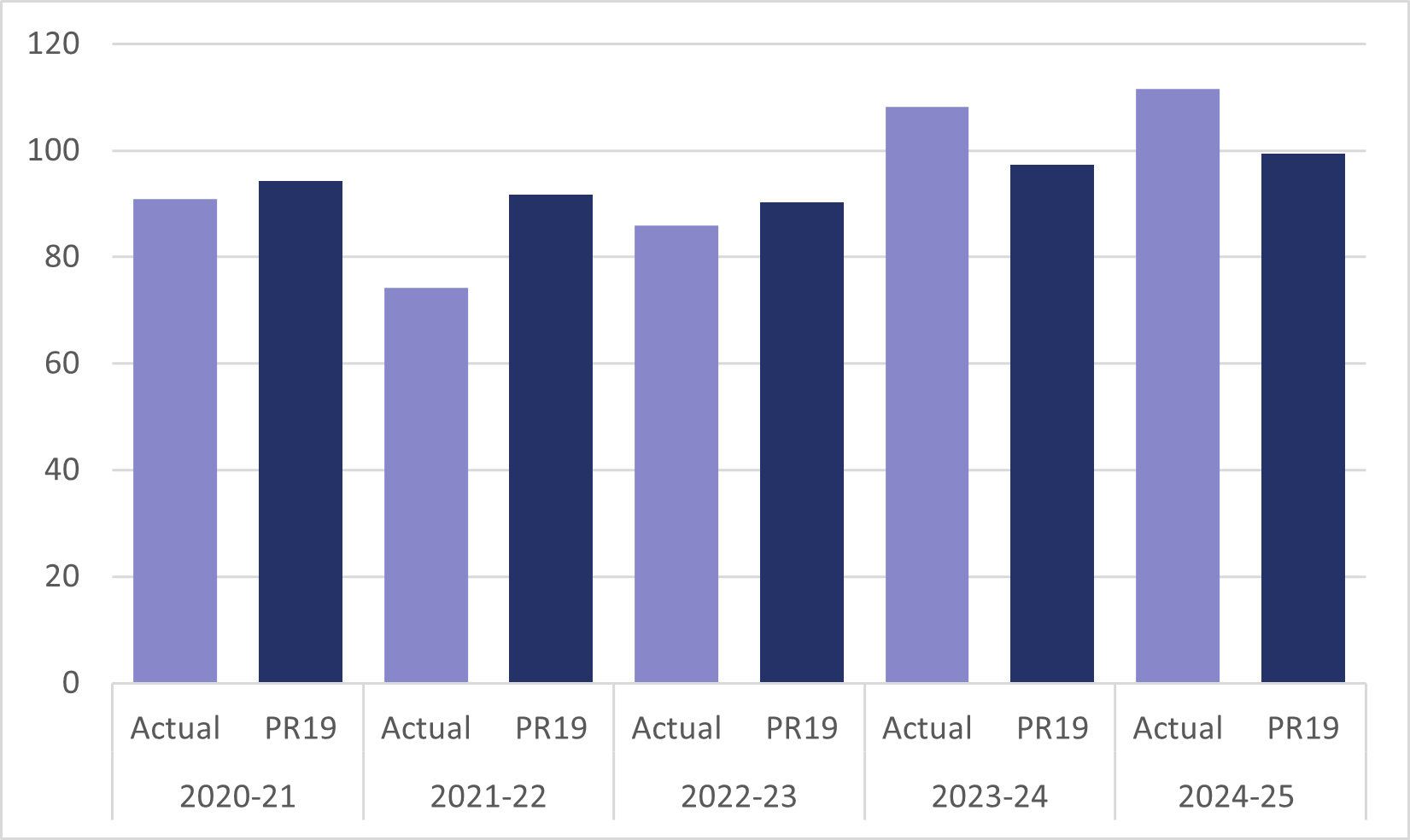

Figure 4.1 Route income in CP3 compared to PR19, £million 2024-25 prices

Source: London St. Pancras Highspeed AMAS 2020-21 to 2024-25

As shown in Figure 4.1, income in the first three years of CP3 was overall much lower than budget as a result of reduced number of services in the First Working Timetable from both international and domestic service. The shortfall has been addressed through the volume reopener model. Overall, O&M revenue was higher than PR19 assumptions due to increased recovery on International, domestic and freight services during the last two years of the control period. The impact of the pandemic on London St. Pancras Highspeed’s income was somewhat reduced by the protections embedded within its Concession Agreement. Please see our previous annual reports for further details.

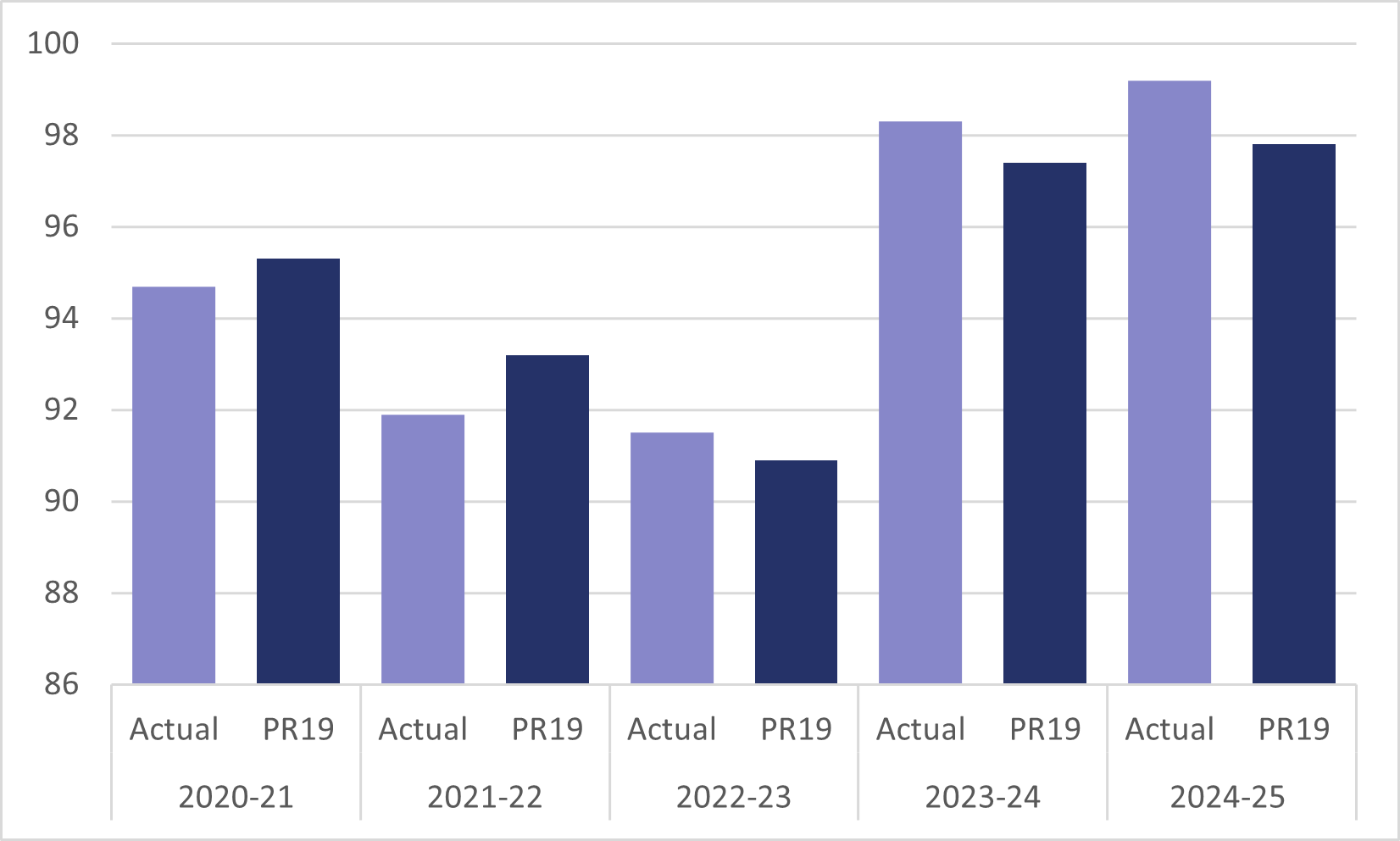

Figure 4.2 Route expenditure in CP3 compared to PR19, £million 2024-25 prices

Source: London St. Pancras Highspeed AMAS 2020-21 to 2024-25

London St. Pancras Highspeed overspent against PR19 over the last three years over CP3 on operations and maintenance. Please refer to previous annual reports for further details.

Efficiency

As part of PR19, we determined an efficient level of cost for the operations, maintenance and renewal of the route infrastructure. The largest element of London St. Pancras Highspeed’s costs is its contract with NR(HS). To demonstrate its progress, NR(HS) reports to us using a “fishbone” analysis which includes:

- efficiencies;

- headwinds (unplanned cost increases due to external factors such as the pandemic);

- tailwinds (unplanned cost decreases due to external factors);

- scope changes (planned changes to levels of work undertaken); and

- input prices (inflationary effects from increases or decreases in costs above general CPI inflation).

NR(HS) has reported net efficiencies of £4m for the final year of CP3 against the target set at PR19 of £3.4m (2024-25 prices). This includes staff related savings, which results from the implementation of a new target operating model by NR(HS). It also includes some offsetting headwinds such as a £0.5m increase related to additional weld repairs on the route.

At PR19, we accepted NR(HS)’s plan to increase efficiency by 6.7% across the five years of CP3. NR(HS) has outperformed on its core efficiency commitments for CP3 and reported net efficiency savings of £17m against the PR19 CP3 target of £11m (2024-25 prices).

Route escrow account

Some of London St. Pancras Highspeed’s access charges are paid into an escrow account to fund current and future renewals of the route. This fulfils a similar function to the Regulatory Asset Base in other regulated utilities by spreading these costs over the long term to ensure that users of the railway pay their fair share.

The balance on the route escrow account (excluding investments) on 31 March 2025 was £196.7m. The escrow balance increased by £36.7m in the year due to:

- £43.1m of payments into the escrow account. This is an increase of £14.2m against the PR19 forecast. Some of this over-recovery relates to the ‘payment holiday’ following the pandemic, which is to be repaid within CP3. These funds are part of the OMR charges paid by operators and are designed to finance future renewals of the HS1 route. The collected amounts are deposited into the escrow account each quarter (similarly the stations long term charges (LTCs) are deposited into ring-fenced escrow accounts for each station each quarter).

- £13.6m was withdrawn to pay for renewals delivery, £3.8m less than forecast at PR19 due to less renewal work being undertaken than planned (see asset management section for more details).

- £7.2m of interest earned in the year which was £6m more than forecast.

Funds invested as at year end for the route were £0, with all investments and interest returning to the current account by the end of the control period as required by the Concession Agreement.

Station charges

Stations renewals charges, referred to as the Long-Term Charge for each station, were set by DfT at PR19. These are set per station so do not vary by traffic volume; income therefore matched forecasts for each station: £7.9m for St. Pancras, £1.7m for Ebbsfleet; £1.6m at Stratford International and £0.9m at Ashford International.

We do not regulate London St. Pancras Highspeed’s operations and maintenance spend for stations, which is set on an annual basis in a process run by the infrastructure manager with the train operators that use its stations. We understand that London St. Pancras Highspeed spent around £38m on these costs in the year, against a budget of £41.9m.

Stations escrow accounts

Operator charges are paid into an escrow account to fund current and future renewals for each of the four stations: London St. Pancras International, Stratford International, Ebbsfleet international and Ashford International.

The balance across all the stations escrow accounts (excluding investments) on 31 March 2025 was £90m, £56m higher than on 31 March 2024. The escrow balances comprise:

- £15.4m income into the escrow accounts through long term charges for each station;

- £4.2m withdrawn to pay for renewals delivery; and

- £4.1m of interest earned in the year.

Funds invested as at year end for the stations are £0. The stations escrow funds have been invested on the same basis as route.

London St. Pancras Highspeed has been seeking to maximise interest earned on the route and station escrow accounts, over retaining cashflow availability for renewals, since December 2021. This year,

London St. Pancras Highspeed and DfT worked together to allow for the investment of these funds in a wider range of institutions and continue to explore opportunities to further help narrow the gap between interest earned and inflation through changes to the Concession Agreement requirements on authorised investments.

Overview of London St. Pancras Highspeed’s statutory financial statements

London St. Pancras Highspeed made a profit after tax of £121.7m this reporting year (up from £101.6m in the previous year) with earnings before interest, tax, depreciation and amortisation of £107.3m (£101m in the previous year). Its net assets increased to £612.1m due to reported profit and servicing of debt.

The ratio of cash available to service annual debt interest and principal payments (DSCR) for 1st April 2024 - 31st March 2025 was 1.47x (noting this was 1.51x in the previous reporting year).

London St. Pancras Highspeed remained above its debt-service cover ratio (DSCR) covenant lock-up level of 1.20. The lock-up level is a restriction of distributions. Until DSCR recovers to above the lock-up threshold, any cash generated in the period that was planned to be paid out to shareholders, must instead be set aside for debt service.